GTA: Private Lending Takes 20% Market Share in Q2 of 2018

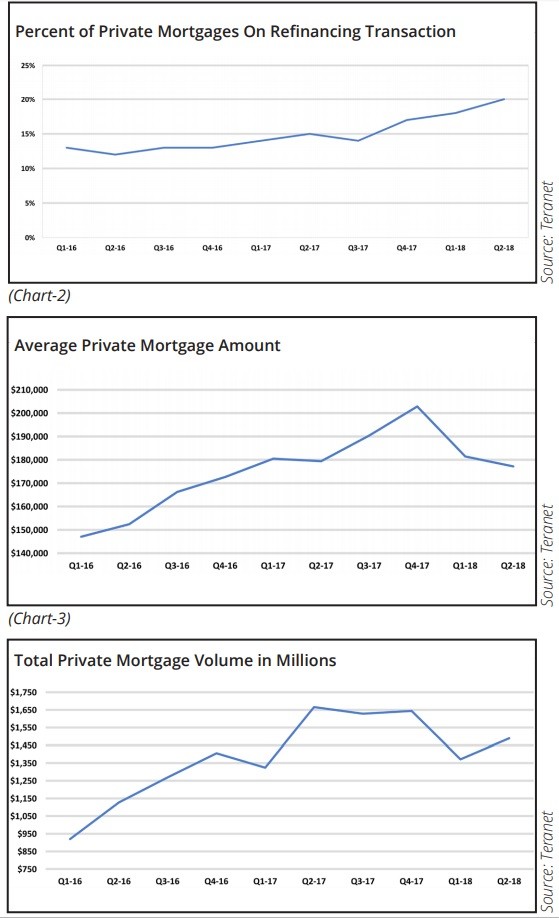

According to a joint study by Teranet and Realosophy, 20% of refinances during the second quarter of 2018 were with private lenders.

“The most likely reason is B-20,” said John Pasalis, president of Realosophy. “Generally, if people are going there, with the increase we’ve seen, it’s because it’s tougher to qualify for a refinance at a traditional bank.”

The study also found that refinances in the private channel jumped 67% in the second quarter compared to the same period a year earlier. That, furthermore, indicates overleveraged borrowers, not all of whom have bruised credit and paltry incomes.

“I was at a conference recently for mortgage brokers specializing in private lending, and they said that a a lot of these people have great jobs and make a lot of money, but they’re have trouble making ends meet,” continued Pasalis. “Whether they’re overspending or have more debt, people are having a hard time financially and need to fill the gap.”

Laura Martin, COO of Matrix Mortgage Global and director of Private Lending Hub, says some brokers choose to disregard the necessity, not to mention benefit, of putting clients in private mortgages, but that the report clearly signifies the importance of the channel.

“It’s impossible to keep denying the fact that there’s a need for private funds to make up for the 20% decrease in purchasing power caused by the stress test,” she said. “Almost 7% of purchases require private financing in the GTA, and after the drop in values during early 2017, many clients looking to finance new builds were left out by their banks and able to save their deposits and close because of private financing.”

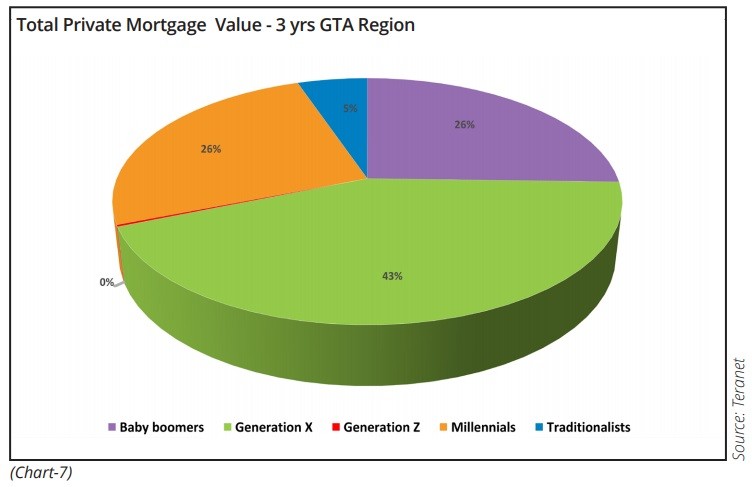

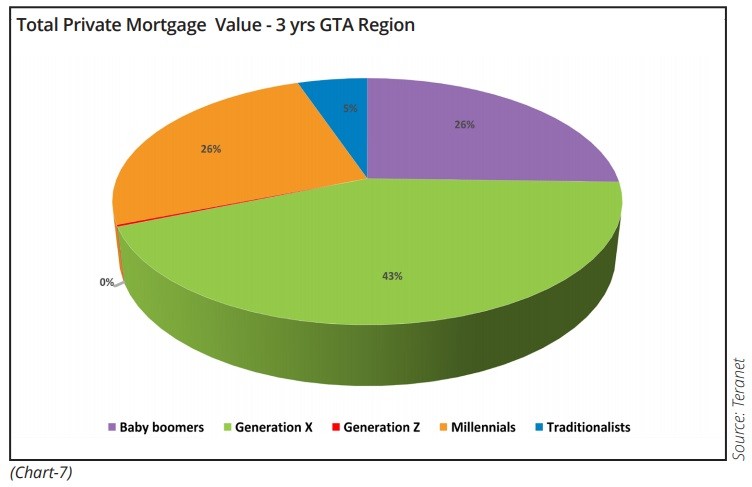

Martin resents the stigma surrounding private financing—a stigma caused by a few predatory lenders. She notes that Generation Xers are the highest recipients of private financing for either construction or extensive renovations.

“Private lenders are more willing than banks to do construction loans,” she said.

Without a doubt, private lenders fulfill a gap in the market—one that opened wider on January 1. However, there has been much talk about further regulation this time targeting alternative lenders, and that makes Pasalis uneasy.

“It just assumes there will be a lot of private money available, and if it isn’t, a lot of homeowners will have to sell their houses,” he said. “ If we see more regulation, this will happen 100%. If house prices don’t rise very much, are investors going to want to take money off the table? It doesn’t mean there won’t be cash; there will always be cash, and probably at a higher interest rate.”

Pasalis notes that one of the private channel’s saving graces is that with increased competition has come competitive interest rates among lenders.

Reference : https://www.linkedin.com/pulse/gta-private-lending-takes-20-market-share-q2-2018-laura-martin/?published=t